After the US stock market closed on Thursday, three more high-profile companies released their earnings reports. (As this public account does not involve any topics related to investment or investment advice, company discussions are limited to business operations; financial performance analysis is cited below only for reference).

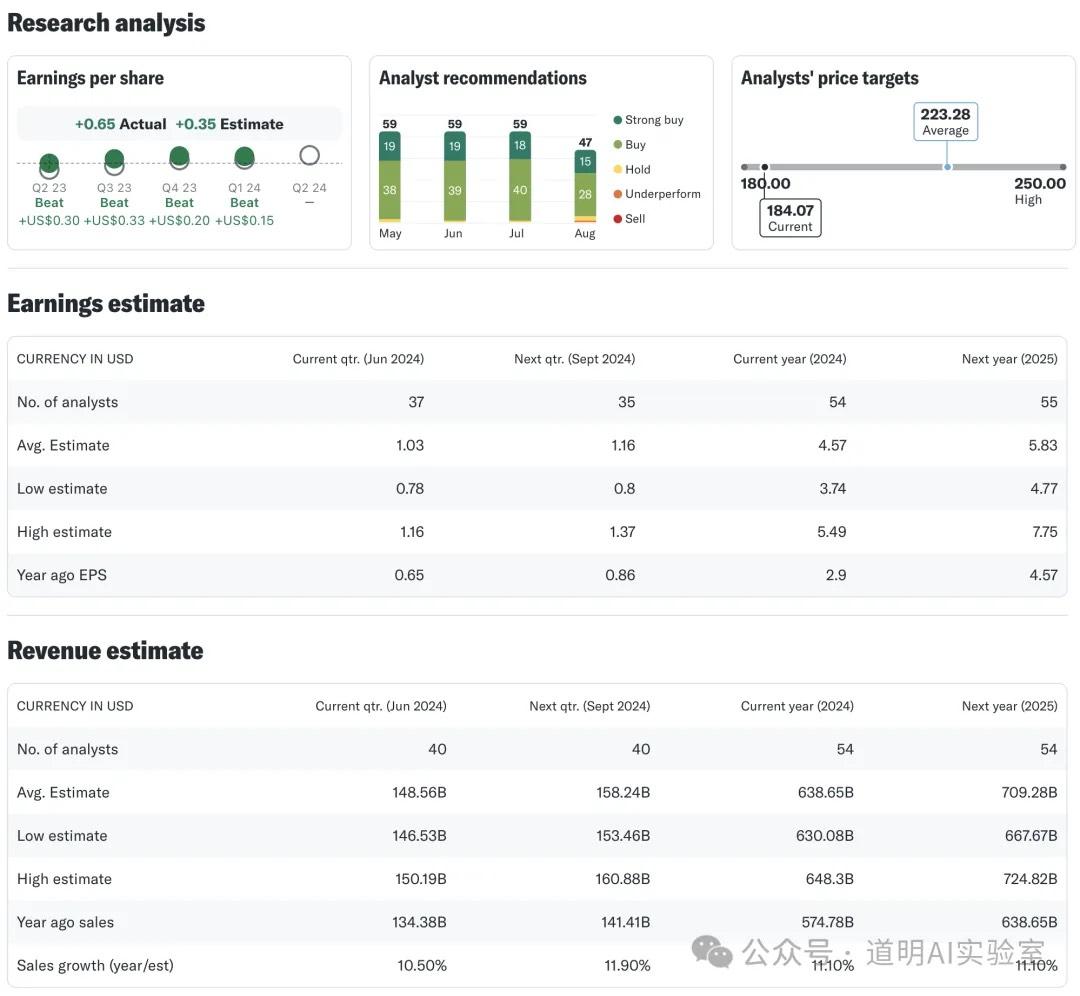

Apple (AAPL) sales growth turned positive year-over-year, with iPad performance significantly exceeding market expectations.

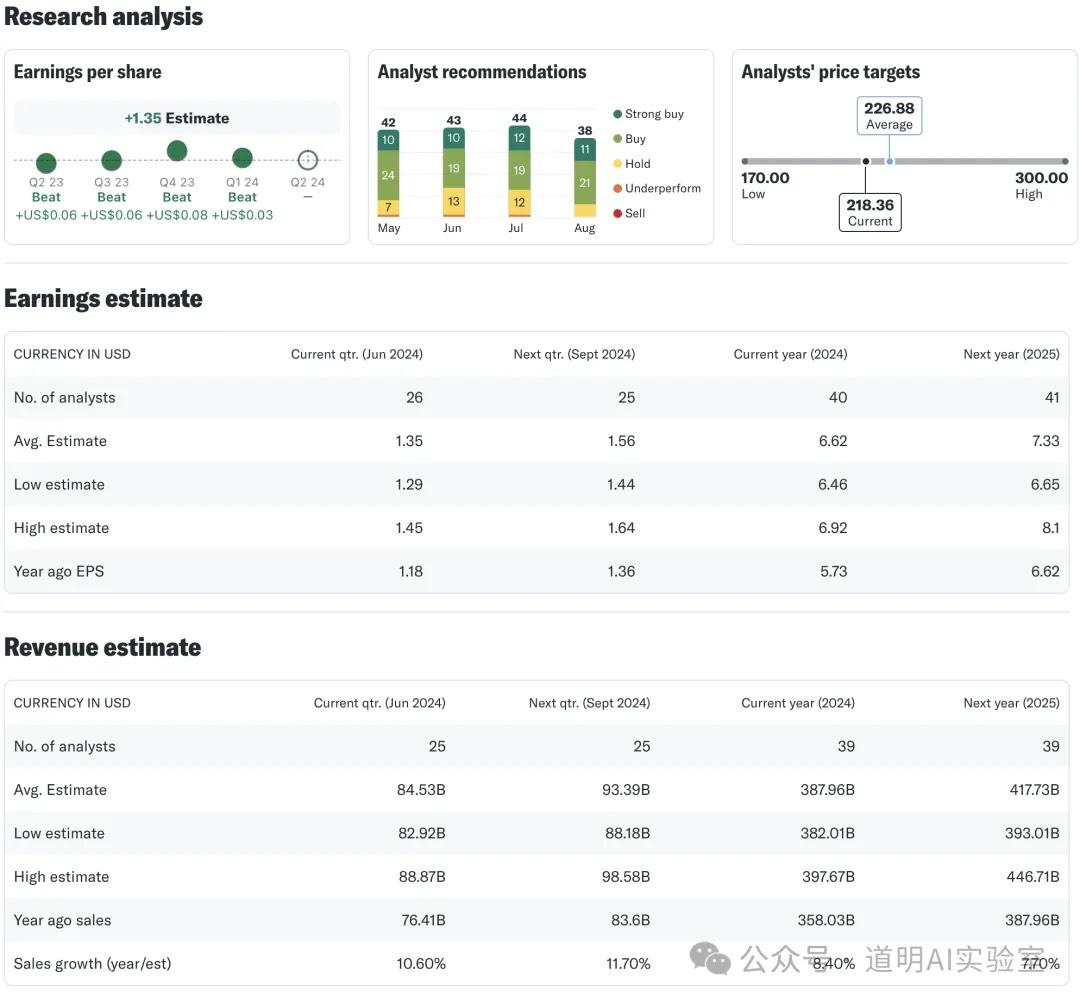

Yahoo Finance: Apple

https://sg.finance.yahoo.com/quote/AAPL/analysis/

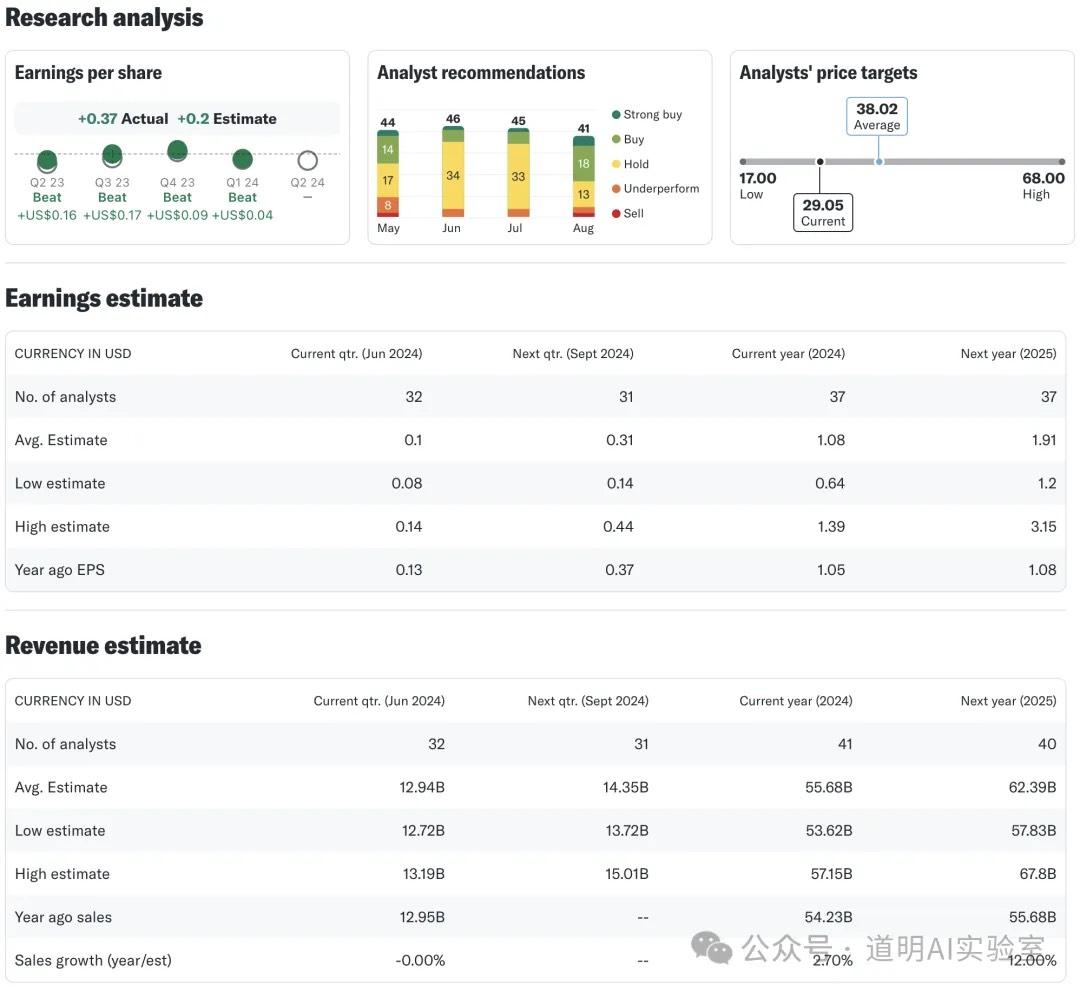

Amazon (AMZN) sales fell short of expectations, but its cloud business (AWS) exceeded expectations.

Yahoo Finance: Amazon

Intel (INTC) not only missed expectations but also provided a very pessimistic outlook, announcing a $10 billion cost-reduction plan and 15,000 layoffs.

Yahoo Finance: Intel

https://sg.finance.yahoo.com/quote/INTC/analysis/

Regarding the businesses themselves, Apple's sales recovery, AWS's growth acceleration, and Intel's struggle could have been predicted with relative certainty. These are not just reflections of a single quarter's performance but manifestations of shifts in core competitiveness, user bases, and business layouts amid the AI wave that began last year.

Objectively speaking, there is a gap between the performance of these three companies and the general perception of users in China:

Many think the iPad is redundant—even if the iPad Pro is powerful, it's so expensive, who buys it? In fact, the iPad user base is highly sticky. In many professional and educational fields, the iPad is essentially the only choice, with Android barely a factor.

For many enterprises, AWS remains the best among the "Big Three" clouds and still holds the highest market share. In an era where models are no longer scarce, AWS's one-stop service capabilities and relatively neutral positioning are advantageous. Among the three major cloud businesses, a year and a half into the AI boom, only Microsoft Azure fell below expectations (though this doesn't imply a lack of demand, as analyzed previously in the post "Brief Commentary on Microsoft Earnings Numbers").

By now, one could say the "road to AGI" has hit some hurdles—computing power, data, and even questions about the Transformer architecture. However, even what current models can achieve is enough to change how many industries operate. Reconstruction based on computation is advancing rapidly, and infrastructure investment won't stop anytime soon. What if there is another breakthrough in models during this process? Market expectations are really just about timing. Since the market can drop 5% one day, rise 10% the next, and drop 5% again on the third, it shows that market volatility is excessive compared to actual industry trends.

Over the past year, I've encountered many optimistic views on Intel and even constantly questioned if I was missing something. But at this stage, perhaps only the top player in each segment can survive. Even ignoring the long-term trend of ARM replacing X86, a bleeding Intel seems to be in worsening condition and is increasingly becoming an effective choice for hedging market risk against AMD.

Returning to Apple, I make no secret of my long-term bullish stance on Apple benefiting from this AI boom. Even if we discuss AI fairness, it's undeniable that while the percentage of "true AI users" (who drive revenue) may be low, their revenue contribution will likely follow an extreme distribution even more lopsided than the 80/20 rule. This is almost inevitable. I like looking at simple data: while Mac accounts for less than 10% of all PCs, it occupies nearly half the market in university campuses and professional fields (including in China). These sectors are the primary source of "true AI users."

The tech earnings season is drawing to a close, with only one major announcement remaining: NVIDIA. Over the past month, I've seen implied volatility for options on companies like Apple, Microsoft, and Google surge from around 20% to over 100%. This is surely making history: tech companies are surrounded by a crowd of "madmen," while the market is filled with greed and fear. Thus, trading has become increasingly disconnected from fundamental analysis—as perhaps it should be.

Note: This piece was completed after the US market close. I hesitated for a few hours but finally decided to post it. I don't have a great feeling about it, because of that increasingly blurred line.