The market is closely watching Microsoft's earnings, with the primary focus on Azure cloud growth—specifically growth driven by AI. Everyone is anxious about one question: can massive capital expenditure actually drive revenue growth?

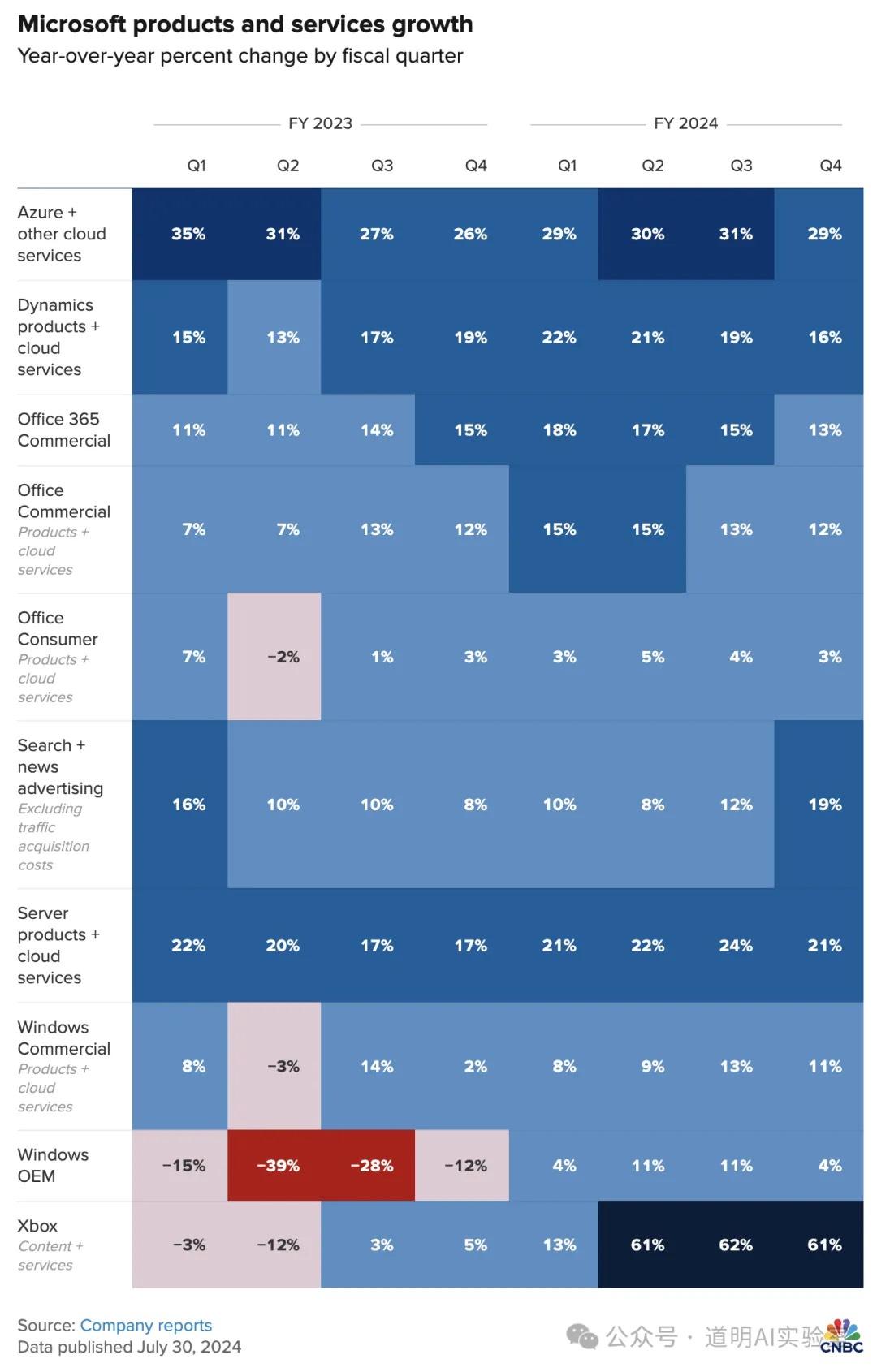

The answer seems somewhat disappointing, but that isn't the whole story. While reviewing market commentary, I saw a chart from CNBC that illustrates the situation perfectly, so I have included it here:

Breaking it down by business segment, Azure's growth has not maintained its previous momentum. Year-over-year (YOY) growth dropped to 29% from over 30% in the previous two quarters, which is the primary reason for the stock's after-hours decline.

However, this needs to be discussed in three parts. For various reasons, I am only expanding on them briefly in this post:

In fact, a 29% growth rate is still very high. Compared to other business lines, the trend of decelerating quarter-over-quarter growth is even more pronounced. This reflects the current reality for many enterprises: capital expenditure for traditional business is largely giving way to AI infrastructure. This is happening not only in the U.S. but also in Europe. When slowing economic growth combines with the impact of AI, it creates a true dilemma for modern enterprises. Beyond the numbers, we should focus on how long this state will persist.

The decline in Azure's growth rate is partly due to decreased investment in traditional cloud services and partly due to supply constraints in Azure's AI offerings. Various earnings reports (IBM, the unlisted Databricks, etc.) tell another story: AI demand remains extremely strong, but supply still cannot keep up. Consequently, we saw AMD—which released earnings on the same day—raise its full-year guidance for its data center business (primarily MI300 GPUs), and we also see Microsoft increasing its purchases of the MI300. Therefore, the more likely story for Azure is that they are facing expansion pressures caused by insufficient supply.

Looking back at Google's earnings from last week, Google Cloud's growth exceeded expectations. This suggests that while Microsoft gained a significant first-mover advantage on Azure due to its relationship with OpenAI, as OpenAI's lead gradually diminishes (with the release of GPT-4o-mini and the fading of the OpenAI "halo"), user choices among cloud service providers will become more balanced.

I have discussed these three stories offline over the past quarter.