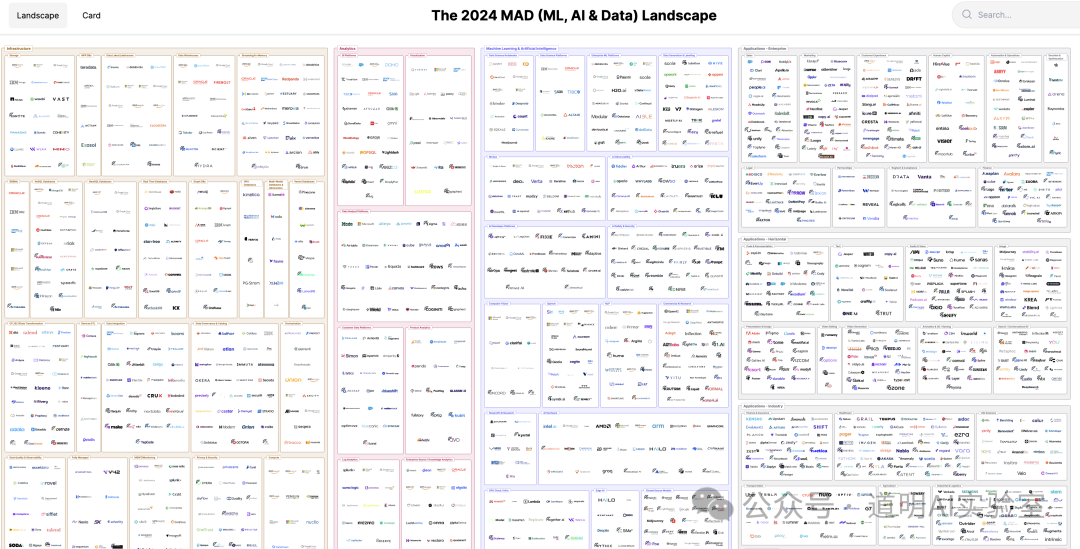

First Mark has updated its 2024 MAD (Machine Learning, AI, Data Science) landscape and included an analysis report.

Visually, it is a landscape map filled with company logos. According to First Mark, a total of 2,011 logos were included this year, an increase of 578 compared to last year's 1,416.

Source: https://mad.firstmark.com

First Mark's analysis report link is https://mattturck.com/MAD2024/. I have placed a Chinese summary at the end of this article.

I took some time to scrape the landscape map and its underlying data for a brief analysis. Out of respect for intellectual property, I cannot provide detailed raw data. Instead, I will offer a simple analysis based on the data and share some of my findings and conclusions.

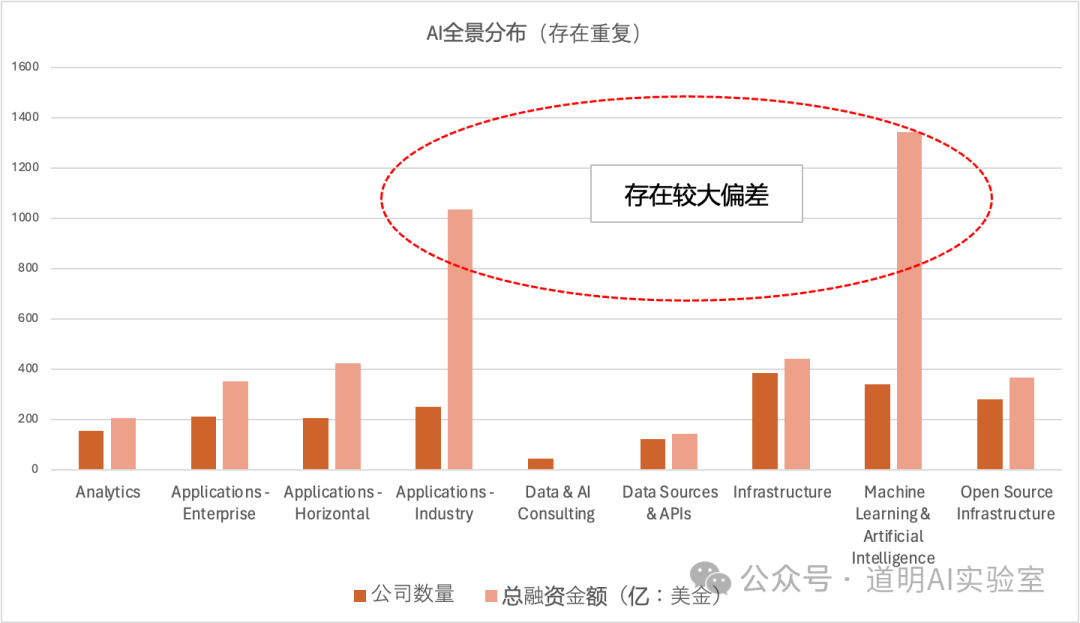

Firstly, I only obtained 1,993 entries, not the 2,011 announced in the news blog, but I believe this gap does not affect the overall conclusion. Of course, because many companies belong to multiple categories and large corporations have different product lines, even among the 1,993 entries, there is significant duplication from a company-wide perspective.

Secondly, according to First Mark's primary classifications, I counted the number of logos and the total funding amounts (there were actually only 1,364 funding records; many giants like IBM, HP, Google, Microsoft, and AWS do not have these specific funding records, so this coverage is actually quite representative). Even with some double-counting due to the reasons mentioned above, the changes in distribution are easy to see.

Looking at specific categories, although "Applications—Industry" and "Machine Learning & AI" do not have the highest number of companies, their funding amounts stand out significantly. In reality, there is some data margin of error here:

- In "Industry Applications," the data includes "Uber," which has a funding amount of $15 billion.

- In First Mark's data, companies like OpenAI are recorded five times under different names, but the funding amount is listed as $14 billion each time. The same applies to Claude's parent company Anthropic, and Inflection, which was recently acquired by Microsoft.

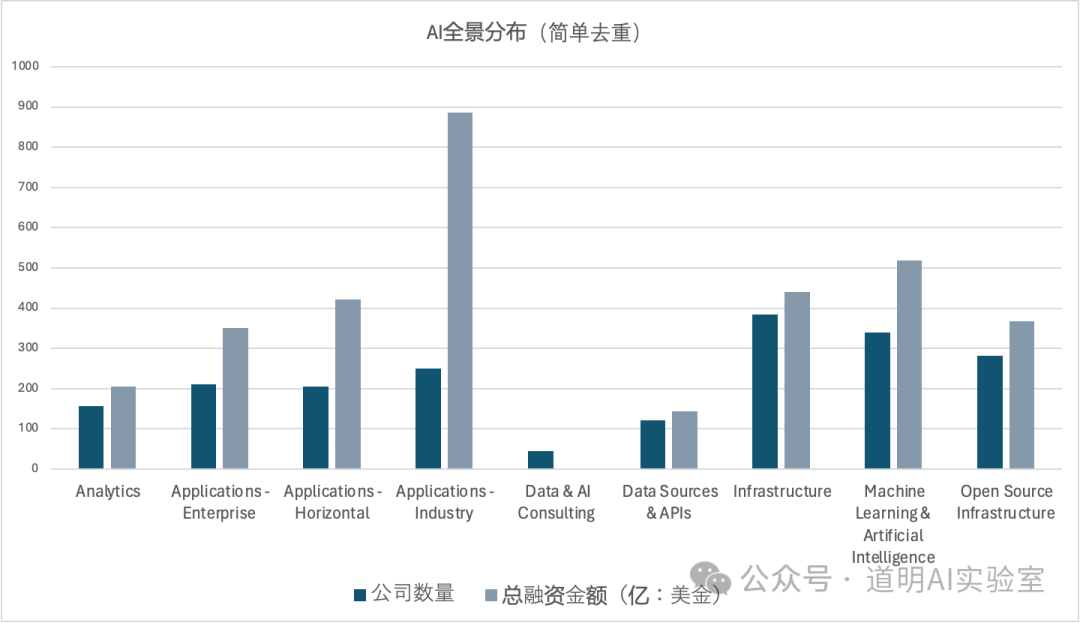

- After making simple corrections for these high-impact data points, the results are as follows:

Clearly, the "real" funding amount for the "Machine Learning & AI" category is no longer as disproportionate, but the "funding per company" ratio remains quite high. In fact, considering there is a group of giants involved (whose specific funding is recorded as 0), this field remains a true "capital sink."

It is worth noting that the application sector remains more attractive for funding. In fact, B2B (Industry and Enterprise) has a stronger capital absorption capacity than B2C (Horizontal). However, as the name suggests, B2C is already "above the waterline" and gets more attention, while B2B is largely hidden beneath the surface, known to few.

If we look at secondary classifications, within the "Industry" category, Healthcare, Life Sciences, and Space Technology account for a high proportion. This was also evident in NVIDIA's recent GTC conference. Technological progress in these fields may offer more tangible value.

Finally, I originally expected that with the AI boom, many companies founded after 2023 would have entered the public eye, but that is not entirely the case.

The number of logos for companies founded after 2023 included in the landscape is 55. After deduplication (Mistral appears four times in different forms, 01 and Yi, xAI and Grok), it is roughly 50. Considering the empirical value of a "two to three-year average lifespan for startups," this number is actually quite low (representing no more than 10% of the total companies included).

AI entrepreneurship is definitely not an easy business.

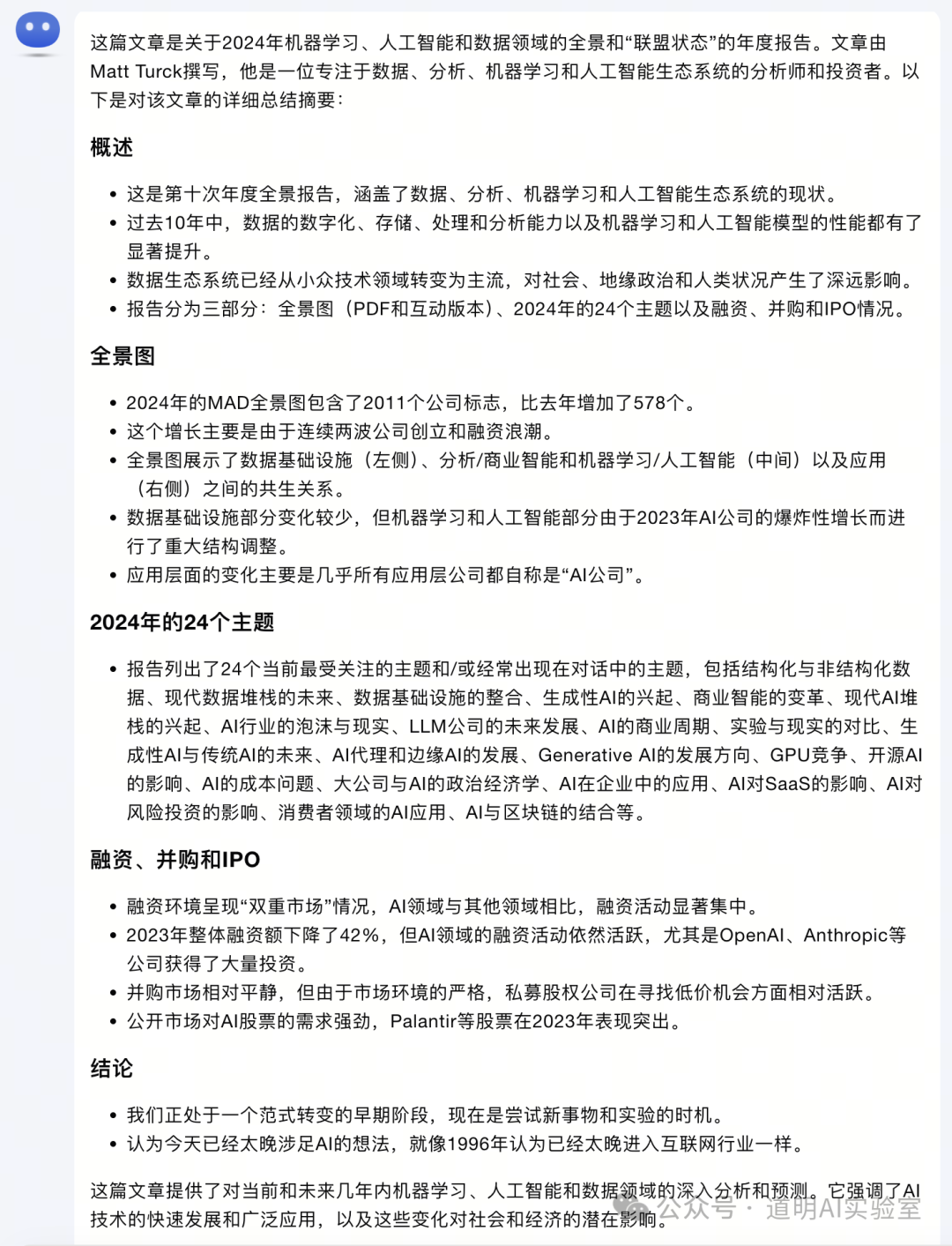

Lastly, as mentioned at the beginning, First Mark released an analysis. I used Kimi Chat to summarize the content, and the results are below.

Despite some flaws, First Mark has done something truly great and has persisted for a long time. Today's brief review is just the tip of the iceberg of the conclusions and insights that can be drawn from the data.

More in-depth analysis and discussion might be more appropriate for offline settings.